策略架构¶

- 策略的固定格式

- 一个经典的商品期货策略架构

- 第 4 行~第 7 行是整个程序的主入口函数

- 计算机是从第 4 行开始执行代码的

- 紧接着直接执行第 5 行,就进入了无限循环

- 然后在无限循环里面一直执行策略逻辑函数(onTick)和休眠函数(Sleep)

- onTick 函数也就是第 1 行的代码

- 可以在第 2 行编写策略逻辑

- 在循环中,程序的执行速度是非常快的,使用休眠函数(Sleep)可以让程序暂停一会,下面的代码 Sleep(500) 就是每循环一次,就休眠 500 毫秒

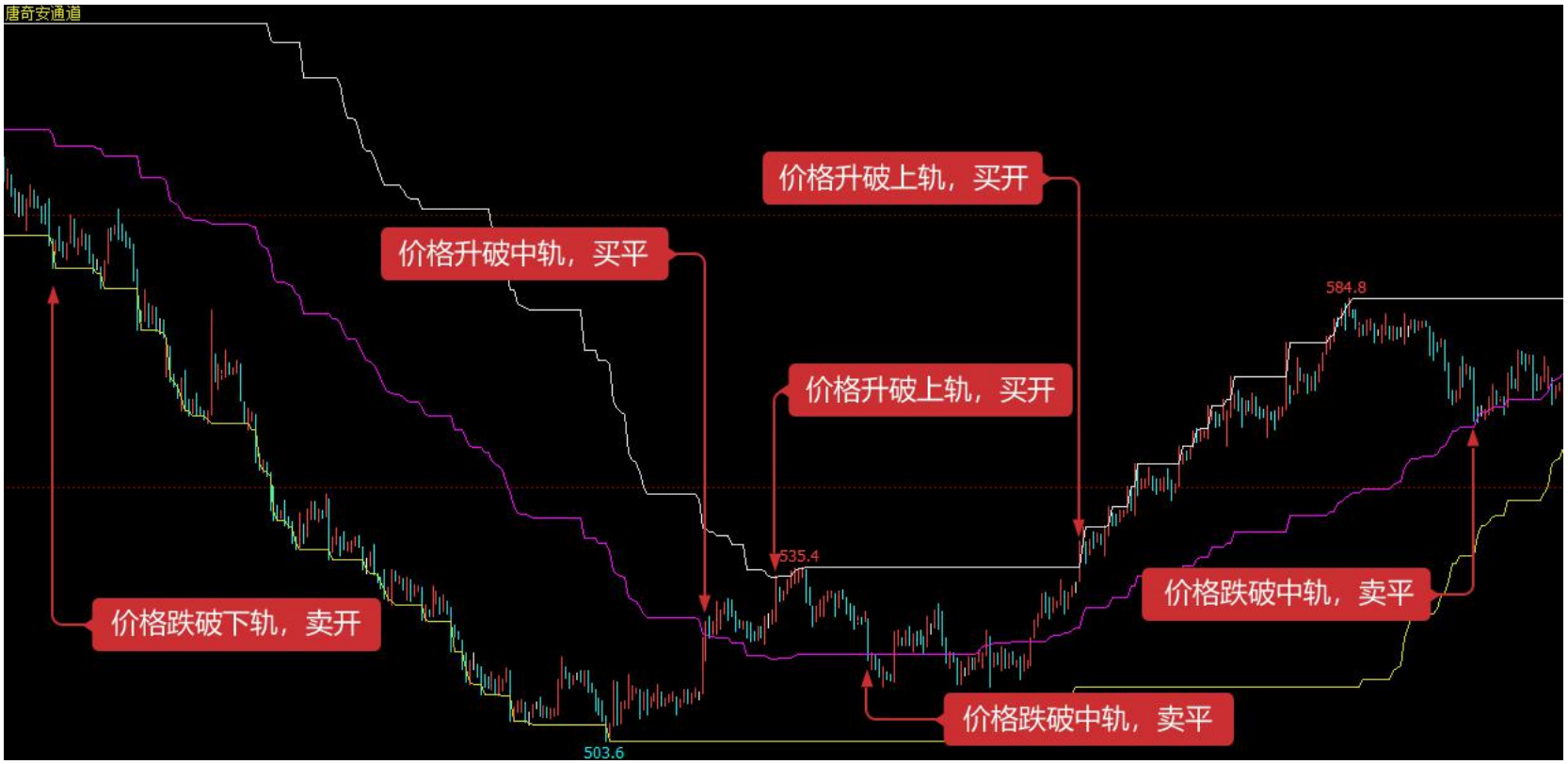

唐奇安通道策略规则¶

- 突破型交易策略适应于走势比较流畅的交易品种,最常见的突破交易方式就是,利用价格与支撑和阻力的相对位置关系,来判断具体交易买卖点位

- 唐奇安通道策略也正是基于这个原理

- 唐奇安的价格通道是根据一定期间内的最高价格与最低价格构建的

- 计算最近 50 根 K 线最高价的最大值,形成上轨

- 计算最近 50 根 K 线最低价的最小值,形成下轨

- 默认是 $20$ 个周期内的最高价和最低价来显示市场价格的波动性

- 当其通道窄时表示市场波动较小

- 反之通道宽则表示市场波动较大

- 信号

- 如果价格升破上轨时,就是买入信号

- 如果价格跌破下轨时,就是卖出信号

- 一般情况下,价格很少同时升破和跌破上下通道线

- 大多数情况下,价格是沿着上轨或下轨单边运动,或者在上轨和下轨之间运动的

唐奇安通道计算方法¶

- 直接使用API获取指定周期内的最高价或最低价

def main() exchange.SetContractType("rb888") # 设置品种代码 while True: # 进入循环 records = exchange.GetRecords() # 获取K线数组 upper = TA.Highest(records, 50, 'High') # 获取50周期最高价的最大值 lower = TA.Lowest(records, 50, 'Low') # 获取50周期最低价的最小值 middle = (upper + lower) / 2 # 计算上轨和下轨的均值 Log("上轨", upper) # 把上轨的值打印到日志中 Log("下轨", lower) # 把上轨的值打印到日志中 Log("中轨", middle) # 把上轨的值打印到日志中

策略逻辑¶

- 当价格自下而上突破上轨,即突破上方压力线时,我们认为多方力量正在走强,一波上涨行情已经形成,买入开仓信号产生

- 当价格自上而下跌破下轨,即跌破下方支撑线时,我们认为空方力量正在走强,一波下跌趋势已经形成,卖出开仓信号产生

- 如果买入开仓后,价格又重新跌回到唐奇安通道中轨,我们认为多方力量正在走弱,或者空方力量正在加强,卖出平仓信号产生

- 如果卖出开仓后,价格又重新涨回到唐奇安通道中轨,我们认为空方力量正在走弱,或者多方力量正在加强,买入平仓信号产生

买卖条件¶

- 多头开仓:如果无持仓,并且收盘价大于上轨

- 空头开仓:如果无持仓,并且收盘价小于下轨

- 多头平仓:如果持多单,并且收盘价小于中轨

- 空头平仓:如果持空单,并且收盘价大于中轨

策略代码实现¶

第一步:使用交易类库¶

- 使用发明者量化工具的 CTA 策略框架

- 这是一个固定的代码格式

def main():

while true:

obj = ext.NewPositionManager() # 使用交易类库

# 这里写策略逻辑和下单代码第二步:获取各种数据¶

- 从策略交易逻辑中发现

- 首先需要获取当前的持仓状态

- 然后比较收盘价与布林带指标上中下轨的相互关系

- 最后判断行情是不是即将收盘

获取 K 线数据¶

def main():

exchange.SetContractType("rb888")

while true:

records = exchange.GetRecords() # 获取K线数组

if len(records) < 50:

continue # 跳过本次循环

close = records[len(records)-1].Close # 获取最新K线收盘价- 第 4 行:获取 K 线数组,这是一个固定的格式

- 第 5 行:过滤 K 线的长度

- 因为我们计算 N 周期最高价或最低价,用的参数是50,当 K 线小于 50 根的时候,是无法计算的

- 所以这里要过滤下 K 线的长度,如果 K 线少于 50 根,就跳过本次循环,继续等待下一根 K 线。

- 第 6 行:用代码“ records[len(records) - 1] ”先获取到 K 线数组的最后一个数据

- 也就是最新的 K 线数据

- 这个数据是一个对象,里面包含:开盘价、最高价、最低价、收盘价、成交量、时间等数据

- 既然它是一个对象,那么可以直接用“ .Close ”获取最新 K 线收盘价

获取持仓数据¶

- 持仓信息是量化交易策略中一个很重要的条件

- 当交易条件成立时,还需要通过持仓状态和持仓数,来判断是否下单

- 比如

- 当买入开仓交易条件成立时

- 如果有持仓,就不必再重复下单了

- 如果无持仓,就可以下单

- 当买入开仓交易条件成立时

- 以下是一个获取持仓信息的函数

- 如果是空仓就返回 0

- 如果持多单就返回 1

- 如果持空单就返回 -1

def mp():

positions = exchange.GetPosition() # 获取持仓数据

if len(positions) == 0:

return 0 # 空仓,返回 0

for i in range(len(positions)): # 遍历持仓数组

if (positions[i]['Type'] == PD_LONG) ro (positions[i]['Type'] == PD_LONG_YD):

return 1

elif (positions[i]['Type'] == PD_SHORT) ro (positions[i]['Type'] == PD_SHORT_YD):

return -1

def main():

exchange.SetContractType("rb888")

while True:

records = exchange.GetRecords()

if len(records) < 50:

continue

close = records[len(records)-1].Close

positions = mp() # 获取持仓信息- 第 2 行:创建一个函数,名字是 mp,这个函数没有参数

- 第 3 行:获取持仓数组,这是一个固定的格式

- 第 4 行:判断持仓数组的长度,如果它的长度等于 0 ,那肯定是空仓,所以就返回 0

- 第 6 行:使用 for 循环,开始遍历这个数组

- 接下来的逻辑就已经很简单了

- 如果持多单,就返回 1

- 如果持空单,就返回 -1

- 接下来的逻辑就已经很简单了

- 第 18 行:调用刚才写的获取持仓信息函数 mp()

获取最近 50 根 K 线的最高价和最低价¶

- 在发明者量化工具中,直接使用 “ TA.Highest ” 和 “ TA.Lowest ” 函数就能直接获取,而不用再自己写逻辑计算

def mp():

positions = exchange.GetPosition() # 获取持仓数据

if len(positions) == 0:

return 0 # 空仓,返回 0

for i in range(len(positions)): # 遍历持仓数组

if (positions[i]['Type'] == PD_LONG) ro (positions[i]['Type'] == PD_LONG_YD):

return 1

elif (positions[i]['Type'] == PD_SHORT) ro (positions[i]['Type'] == PD_SHORT_YD):

return -1

def main():

exchange.SetContractType("rb888")

while True:

records = exchange.GetRecords()

if len(records) < 50:

continue

close = records[len(records)-1].Close

positions = mp() # 获取持仓信息

upper = TA.Highest(records, 50,'High') # 获取50周期最高价的最大值

lower = TA.Lowest(records, 50, 'Low') # 获取50周期最低价的最小值

middle = (upper + lower) / 2 # 计算上轨和下轨的均值- 第 19 行:调用 TA.Highest”函数,获取 50 周期最高价的最大值

- 第 20 行:调用“TA.Lowest”函数,获取 50 周期最低价的最小值

- 第 21 行:根据 50 周期最高价的最大值和 50 周期最低价的最小值,计算出平均值

第三步:下单交易¶

- 伪代码

- 如果条件 1 和条件 2 成立,下单

- 如果条件 3 或条件 4 成立,下单

def mp():

positions = exchange.GetPosition() # 获取持仓数据

if len(positions) == 0:

return 0 # 空仓,返回 0

for i in range(len(positions)): # 遍历持仓数组

if (positions[i]['Type'] == PD_LONG) ro (positions[i]['Type'] == PD_LONG_YD):

return 1

elif (positions[i]['Type'] == PD_SHORT) ro (positions[i]['Type'] == PD_SHORT_YD):

return -1

def main():

exchange.SetContractType("rb888")

while True:

records = exchange.GetRecords()

if len(records) < 50:

continue

close = records[len(records)-1].Close

positions = mp() # 获取持仓信息

upper = TA.Highest(records, 50,'High') # 获取50周期最高价的最大值

lower = TA.Lowest(records, 50, 'Low') # 获取50周期最低价的最小值

middle = (upper + lower) / 2 # 计算上轨和下轨的均值

obj = ext.NewPositionManager() # 使用交易类库

if positions > 0 and close < middle: # 如果持多单,且收盘价跌破中轨

obj.CoverAll() # 平掉所有仓位

if positions < 0 and close > middle: # 如果持空单,且收盘价升破中轨

obj.CoverAll() # 平掉所有仓位

if positions == 0:

if close > upper: # 收盘价升破上轨

obj.OpenLong("rb888",1) # 买开

if close < lower: # 收盘价跌破下轨

obj.OpenShort("rb888",1) # 卖开- 第 22 行:使用交易类库,这是一个固定的格式

- 第 23、24 行:这是一个平多单的语句,其中用到了我们之前学过的“比较运算符”和“逻辑运算符”,意思是如果当前持多单,并且收盘价小于中轨,就平掉所有仓位

- 第 25、26 行:这是一个平空单的语句,其中用到了我们之前学过的“比较运算符”和“逻辑运算符”,意思是如果当前持空单,并且收盘价大于中轨,就平掉所有仓位

- 第 27 行:判断当前持仓状态,如果持空仓,才进行下一步

- 第 28、29 行:判断收盘价是否大于上轨,如果收盘价升破上轨,就买入开仓

- 第 30、31 行:判断收盘价是否小于下轨,如果收盘价跌破下轨,就卖出开仓